Form 3520 Late Filing Penalty

Form 3520 Late Filing Penalty - Web the federal district court struck down the irs's imposition of a 35% civil penalty for failing to timely file a form 3520 — an information return used to report, among other things, transactions with foreign trusts — and limited the penalty to a. The maximum penalty is 25% of the amount of the gift. Form 3520 is due at the time of a timely filing of the u.s. If the due date for filing the tax return is extended, the due date Generally, the cp15 states that the taxpayer may submit a reasonable cause statement contesting. Taxpayers should work with their counsel to assess the different strategies and how to proceed on. Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. Web to the extent a taxpayer fails to file a form 3520 where the taxpayer is otherwise required to do so, the taxpayer may receive cp15. Web in particular, late filers of form 3520, “annual return to report transactions with foreign trusts and receipt of certain foreign gifts,” have found it challenging to persuade the irs to even. Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date.

The maximum penalty is 25% of the amount of the gift. Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. Web to the extent a taxpayer fails to file a form 3520 where the taxpayer is otherwise required to do so, the taxpayer may receive cp15. 35% of distributions received from a foreign trust (form 3520); Form 3520 is due at the time of a timely filing of the u.s. Web the federal district court struck down the irs's imposition of a 35% civil penalty for failing to timely file a form 3520 — an information return used to report, among other things, transactions with foreign trusts — and limited the penalty to a. Generally, the cp15 states that the taxpayer may submit a reasonable cause statement contesting. Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. 35% of contributions to a foreign trust (form 3520); When this type of abatement occurs, a 21c letter is issued.

Web the federal district court struck down the irs's imposition of a 35% civil penalty for failing to timely file a form 3520 — an information return used to report, among other things, transactions with foreign trusts — and limited the penalty to a. Form 3520 is due at the time of a timely filing of the u.s. Taxpayers should work with their counsel to assess the different strategies and how to proceed on. Web the form 3520 penalty may be abated (removed) based on the letter alone. Web in particular, late filers of form 3520, “annual return to report transactions with foreign trusts and receipt of certain foreign gifts,” have found it challenging to persuade the irs to even. Web to the extent a taxpayer fails to file a form 3520 where the taxpayer is otherwise required to do so, the taxpayer may receive cp15. Web penalties may be assessed in accordance with existing procedures. Web a penalty applies if form 3520 is not timely filed or if the information is incomplete or incorrect (see below for an exception if there is reasonable cause). 35% of distributions received from a foreign trust (form 3520); Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date.

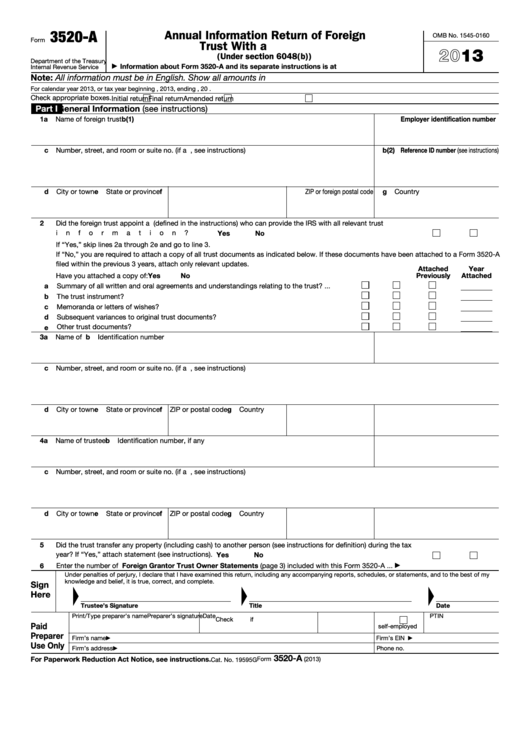

Relief from Filing Forms 3520 and Form 3520A for Some SF Tax Counsel

Web a penalty applies if form 3520 is not timely filed or if the information is incomplete or incorrect (see below for an exception if there is reasonable cause). Web penalties may be assessed in accordance with existing procedures. The maximum penalty is 25% of the amount of the gift. Taxpayers should work with their counsel to assess the different.

Form 3520 Blank Sample to Fill out Online in PDF

Form 3520 is due at the time of a. When this type of abatement occurs, a 21c letter is issued. Web if you file form 3520 late, or if the information provided is incomplete or incorrect, the irs may determine the income tax consequences of the receipt of such foreign gift or bequest and you may be subject to penalties.

Has the IRS Assessed You a Penalty for a Late Filed Form 3520A? You

Generally, the cp15 states that the taxpayer may submit a reasonable cause statement contesting. If the due date for filing the tax return is extended, the due date Web the federal district court struck down the irs's imposition of a 35% civil penalty for failing to timely file a form 3520 — an information return used to report, among other.

The Tax Times Foreign Trust Form 3520A Filing Date Reminder & Tips To

Web if you file form 3520 late, or if the information provided is incomplete or incorrect, the irs may determine the income tax consequences of the receipt of such foreign gift or bequest and you may be subject to penalties under section 6039f(c) if. The maximum penalty is 25% of the amount of the gift. Web the form 3520 penalty.

Penalty for Late Filing Form 2290 Computer Tech Reviews

The maximum penalty is 25% of the amount of the gift. If the due date for filing the tax return is extended, the due date Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. 35% of contributions to a foreign trust (form.

Form 3520 Annual Return to Report Transactions with Foreign Trusts

When this type of abatement occurs, a 21c letter is issued. Web to the extent a taxpayer fails to file a form 3520 where the taxpayer is otherwise required to do so, the taxpayer may receive cp15. The maximum penalty is 25% of the amount of the gift. The maximum penalty is 25% of the amount of the gift. 35%.

Are Distributions From Foreign Trust Reportable on Tax Return?

If the due date for filing the tax return is extended, the due date Web if you file form 3520 late, or if the information provided is incomplete or incorrect, the irs may determine the income tax consequences of the receipt of such foreign gift or bequest and you may be subject to penalties under section 6039f(c) if. Form 3520.

A District Court Determines that a Sole Beneficiary of a Foreign Trust

Taxpayers should work with their counsel to assess the different strategies and how to proceed on. Web the form 3520 penalty may be abated (removed) based on the letter alone. If the due date for filing the tax return is extended, the due date Generally, the initial penalty is equal to the greater of $10,000 or the following (as applicable)..

The Tax Times IRS Sending SemiAutomated Penalties For Late Filed Form

Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. Generally, the initial penalty is equal to the greater of $10,000 or the following (as applicable). Web to the extent a taxpayer fails to file a form 3520 where the taxpayer is otherwise.

Fillable Form 3520A Annual Information Return Of Foreign Trust With

Web the form 3520 penalty may be abated (removed) based on the letter alone. Web penalties may be assessed in accordance with existing procedures. Generally, the initial penalty is equal to the greater of $10,000 or the following (as applicable). When this type of abatement occurs, a 21c letter is issued. Taxpayers should work with their counsel to assess the.

Web A Penalty Applies If Form 3520 Is Not Timely Filed Or If The Information Is Incomplete Or Incorrect (See Below For An Exception If There Is Reasonable Cause).

Web to the extent a taxpayer fails to file a form 3520 where the taxpayer is otherwise required to do so, the taxpayer may receive cp15. Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. Generally, the cp15 states that the taxpayer may submit a reasonable cause statement contesting. When this type of abatement occurs, a 21c letter is issued.

The Maximum Penalty Is 25% Of The Amount Of The Gift.

Form 3520 is due at the time of a timely filing of the u.s. Web the penalty for filing a delinquent form 3520 is 5% of the value of the unreported gift for each month that passes after its due date. Taxpayers should work with their counsel to assess the different strategies and how to proceed on. Web the federal district court struck down the irs's imposition of a 35% civil penalty for failing to timely file a form 3520 — an information return used to report, among other things, transactions with foreign trusts — and limited the penalty to a.

Web In Particular, Late Filers Of Form 3520, “Annual Return To Report Transactions With Foreign Trusts And Receipt Of Certain Foreign Gifts,” Have Found It Challenging To Persuade The Irs To Even.

Form 3520 is due at the time of a. 35% of distributions received from a foreign trust (form 3520); If the due date for filing the tax return is extended, the due date Web penalties may be assessed in accordance with existing procedures.

Generally, The Initial Penalty Is Equal To The Greater Of $10,000 Or The Following (As Applicable).

Web the form 3520 penalty may be abated (removed) based on the letter alone. Web if you file form 3520 late, or if the information provided is incomplete or incorrect, the irs may determine the income tax consequences of the receipt of such foreign gift or bequest and you may be subject to penalties under section 6039f(c) if. 35% of contributions to a foreign trust (form 3520); The maximum penalty is 25% of the amount of the gift.