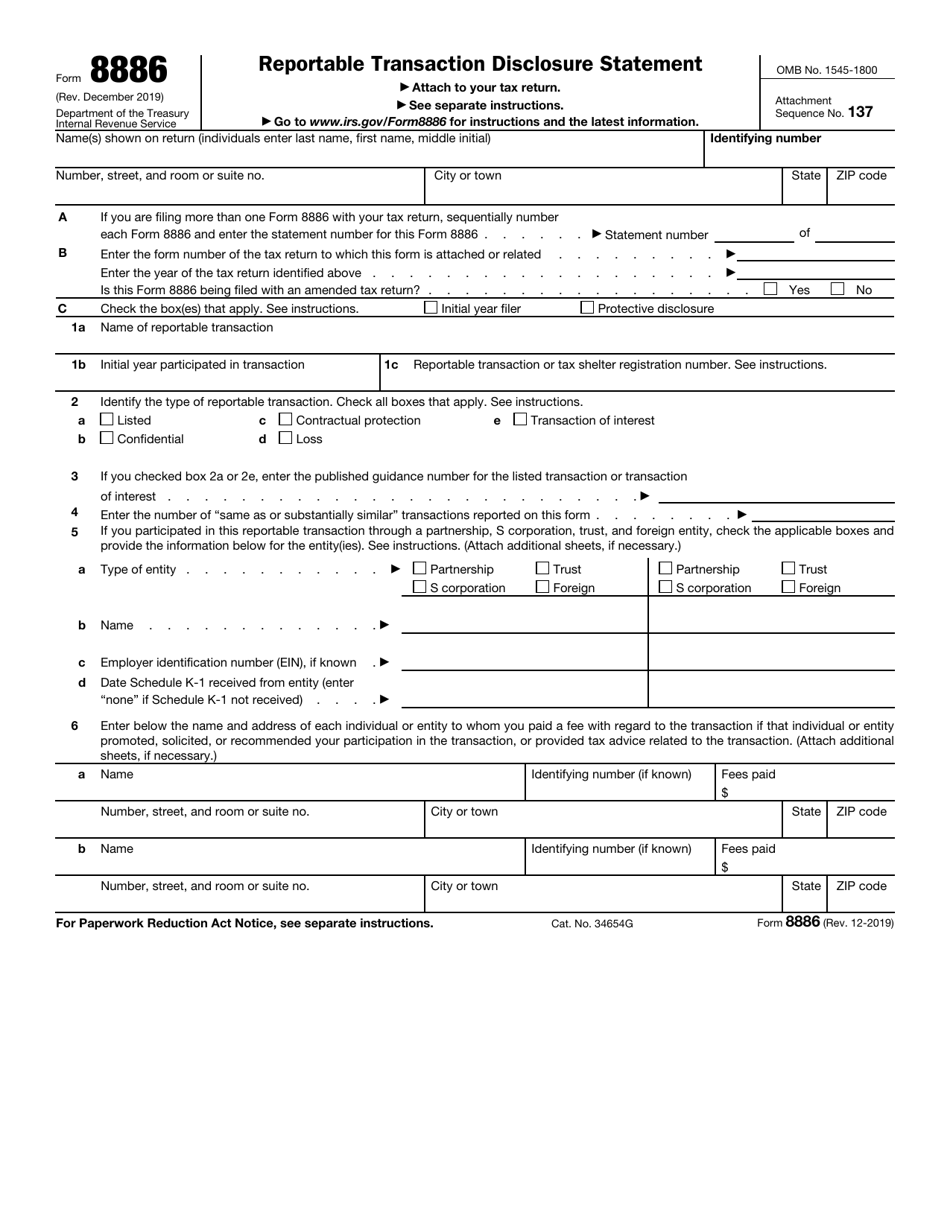

What Is Form 8886

What Is Form 8886 - Does this change affect me? Web use form 8886 to disclose information for each reportable transaction in which participation has occurred. Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction (see item 2 below) and is required to file a federal tax return or information return must file form 8886. Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction and is required to file a federal tax return or information return must file form 8886. Web form 8886 when a taxpayer participates in certain transactions in which the irs has deemed the type of transaction prone to illegal tax avoidance — it is is referred to as a reportable transaction — and the taxpayer may have. However, you may report nonrecognition of gain, tax credits, revenue bulletin. For instructions and the latest information. Web in addition, a report of foreign bank and financial accounts under the bank secrecy act, fincen form 114, must be filed. Describe the expected tax treatment and all potential tax benefits expected to result from the transaction; If a taxpayer entered into a transaction after august 2, 2007, and it later becomes a listed or toi transaction, the taxpayer must file a disclosure with otsa within 90 days.

Generally, form 8886 must be attached to the tax return for each tax year in which participation in a reportable transaction has occurred. Web the form 8886 must reflect either tax consequences or a tax strategy described in the published guidance listing the transaction or designating the transaction as a toi. If a taxpayer entered into a transaction after august 2, 2007, and it later becomes a listed or toi transaction, the taxpayer must file a disclosure with otsa within 90 days. Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction (see item 2 below) and is required to file a federal tax return or information return must file form 8886. Web who must file form 8886? Attach to your tax return. Web in addition, a report of foreign bank and financial accounts under the bank secrecy act, fincen form 114, must be filed. To be considered complete, the information provided on form 8886 must: Describe the expected tax treatment and all potential tax benefits expected to result from the transaction; Does this change affect me?

However, you may report nonrecognition of gain, tax credits, revenue bulletin. Web use form 8886 to disclose information for each reportable transaction in which participation has occurred. Generally, form 8886 must be attached to the tax return for each tax year in which participation in a reportable transaction has occurred. For instructions and the latest information. Web the form 8886 must reflect either tax consequences or a tax strategy described in the published guidance listing the transaction or designating the transaction as a toi. Irc 831(b) captive insurance is considered a listed transaction, requiring form 8886, reportable transaction disclosure statement, to be prepared each year. Web who must file form 8886? Describe the expected tax treatment and all potential tax benefits expected to result from the transaction; Web form 8886 when a taxpayer participates in certain transactions in which the irs has deemed the type of transaction prone to illegal tax avoidance — it is is referred to as a reportable transaction — and the taxpayer may have. Use form 8886 to disclose information for each reportable transaction in which you participated.

Form 8886 Edit, Fill, Sign Online Handypdf

Use form 8886 to disclose information for each reportable transaction in which you participated. Web form 8886 for each reportable exclusions from gross income, updated in future issues of the internal transaction. Attach to your tax return. December 2019) department of the treasury internal revenue service. Web use form 8886 to disclose information for each reportable transaction in which participation.

Form 8886 Edit, Fill, Sign Online Handypdf

Web the form 8886 must reflect either tax consequences or a tax strategy described in the published guidance listing the transaction or designating the transaction as a toi. Web form 8886 when a taxpayer participates in certain transactions in which the irs has deemed the type of transaction prone to illegal tax avoidance — it is is referred to as.

Section 79 Plans and Captive Insurance Form 8886

For instructions and the latest information. Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction and is required to file a federal tax return or information return must file form 8886. Describe the expected tax treatment and all potential tax benefits expected to result from the transaction; However, you may.

Authority for Disallowance of Tax Benefits Restricted Property Trusts

Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction (see item 2 below) and is required to file a federal tax return or information return must file form 8886. Web the form 8886 must reflect either tax consequences or a tax strategy described in the published guidance listing the transaction.

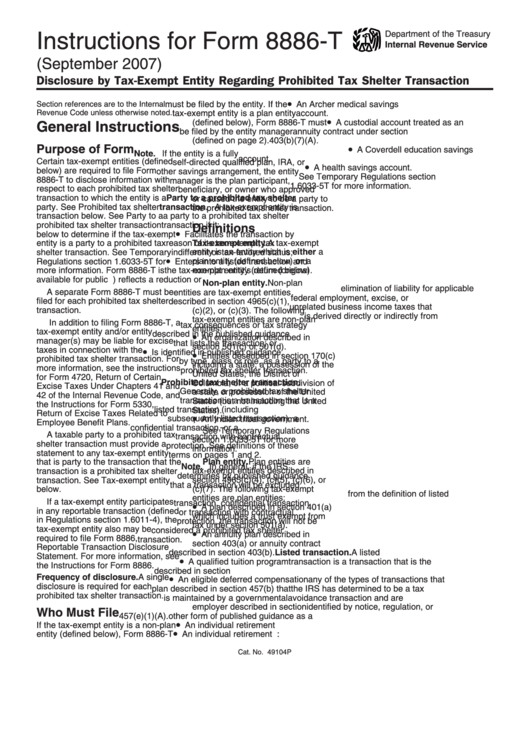

Form 8886T Disclosure by Tax Exempt Entity Regarding Prohibited Tax

Describe the expected tax treatment and all potential tax benefits expected to result from the transaction; Web in addition, a report of foreign bank and financial accounts under the bank secrecy act, fincen form 114, must be filed. Attach to your tax return. However, you may report nonrecognition of gain, tax credits, revenue bulletin. For instructions and the latest information.

Form 8886 Instructions Fill Out and Sign Printable PDF Template signNow

However, you may report nonrecognition of gain, tax credits, revenue bulletin. Web who must file form 8886? Irc 831(b) captive insurance is considered a listed transaction, requiring form 8886, reportable transaction disclosure statement, to be prepared each year. Generally, form 8886 must be attached to the tax return for each tax year in which participation in a reportable transaction has.

Form 8886T Disclosure by Tax Exempt Entity Regarding Prohibited Tax

Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction and is required to file a federal tax return or information return must file form 8886. Web in addition, a report of foreign bank and financial accounts under the bank secrecy act, fincen form 114, must be filed. Web use form.

Form 8886 Reportable Transaction Disclosure Statement (2011) Free

Web use form 8886 to disclose information for each reportable transaction in which participation has occurred. December 2019) department of the treasury internal revenue service. For instructions and the latest information. Does this change affect me? If a taxpayer entered into a transaction after august 2, 2007, and it later becomes a listed or toi transaction, the taxpayer must file.

IRS Form 8886 Download Fillable PDF or Fill Online Reportable

Irc 831(b) captive insurance is considered a listed transaction, requiring form 8886, reportable transaction disclosure statement, to be prepared each year. Web the form 8886 must reflect either tax consequences or a tax strategy described in the published guidance listing the transaction or designating the transaction as a toi. Describe the expected tax treatment and all potential tax benefits expected.

Instructions For Form 8886T Disclosure By TaxExempt Entity

Use form 8886 to disclose information for each reportable transaction in which you participated. Attach to your tax return. Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction (see item 2 below) and is required to file a federal tax return or information return must file form 8886. To be.

Generally, Form 8886 Must Be Attached To The Tax Return For Each Tax Year In Which Participation In A Reportable Transaction Has Occurred.

Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction (see item 2 below) and is required to file a federal tax return or information return must file form 8886. Irc 831(b) captive insurance is considered a listed transaction, requiring form 8886, reportable transaction disclosure statement, to be prepared each year. Web the form 8886 must reflect either tax consequences or a tax strategy described in the published guidance listing the transaction or designating the transaction as a toi. Describe the expected tax treatment and all potential tax benefits expected to result from the transaction;

Does This Change Affect Me?

December 2019) department of the treasury internal revenue service. Web who must file form 8886? Web form 8886 when a taxpayer participates in certain transactions in which the irs has deemed the type of transaction prone to illegal tax avoidance — it is is referred to as a reportable transaction — and the taxpayer may have. For instructions and the latest information.

Use Form 8886 To Disclose Information For Each Reportable Transaction In Which You Participated.

However, you may report nonrecognition of gain, tax credits, revenue bulletin. Web use form 8886 to disclose information for each reportable transaction in which participation has occurred. Attach to your tax return. To be considered complete, the information provided on form 8886 must:

Web Form 8886 For Each Reportable Exclusions From Gross Income, Updated In Future Issues Of The Internal Transaction.

Web in addition, a report of foreign bank and financial accounts under the bank secrecy act, fincen form 114, must be filed. If a taxpayer entered into a transaction after august 2, 2007, and it later becomes a listed or toi transaction, the taxpayer must file a disclosure with otsa within 90 days. Any taxpayer, including an individual, trust, estate, partnership, s corporation, or other corporation, that participates in a reportable transaction and is required to file a federal tax return or information return must file form 8886.